ETF launches are skyrocketing, but the math is brutal: 90% of new active funds operate at a loss while legacy giants take all the cash.

Smaller ETF fund sponsors already know the market is incredibly tough, but recent data reveals a stark reality: product manufacturing has completely decoupled from organic asset gathering. We are currently witnessing a classic “spaghetti on the wall” phenomenon where issuers throw hundreds of niche, active, and derivative-based strategies at the market to see what sticks.

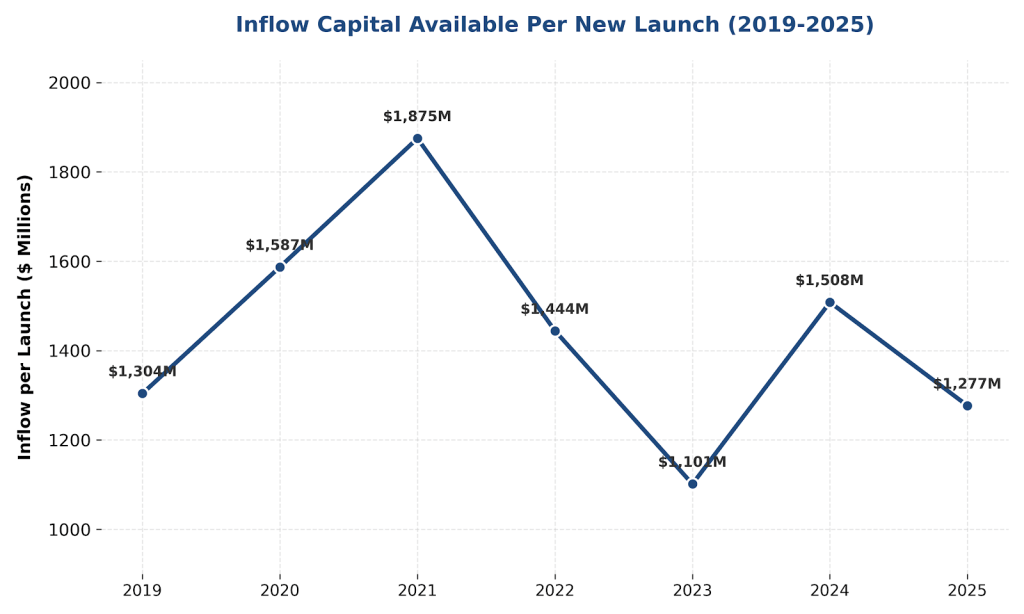

The underlying numbers paint a brutal story. In 2025, issuers rolled out a record-shattering 1,167 new ETFs. Yet, the ratio of annual industry inflows to new product launches has plummeted by over 30% from its post-pandemic peak, dropping from $1.88 billion per launch in 2021 down to just $1.28 billion by 2025.

Where is the money actually going? It is being siphoned directly to the top. A tiny elite of legacy index-tracking giants continues to suck up the lion’s share of investor capital. For instance, Vanguard’s VOO alone swallowed over $113 billion in a single year—capturing more investor cash than hundreds of new active launches combined.

This top-heavy dynamic creates a lethal environment for independent sponsors. While the aggregate average AUM per ETF looks healthy on paper (inflated by mega-caps and a roaring equity bull market), the median fund is starving. Today, nearly 90% of new active ETF launches fail to cross the crucial $50M to $100M operational breakeven threshold within their first year. This means the vast majority are running at a pure loss.

With liquidations climbing back up to 232 per year, the runway for new funds is shorter than ever. For boutique sponsors, survival requires moving away from copycat strategies and focusing on hyper-distribution; otherwise, you’re just adding to the noise on a very crowded wall.